If uncertainty has you feeling anxious and itchy to do something, this episode will show you exactly where to channel that energy — and why the investors who come through periods like this the strongest are the ones who already have a plan in place.

The stock market is bouncing around. The headlines are loud. There are literal wars to worry about. So if you’ve logged into your investment account recently and felt a knot in your stomach, you’re not alone.

In this episode of Money For Life, we cut through the noise to give you a clear-headed, data-backed look at what market volatility actually means for your financial plan. We’re also sharing what you should (and absolutely should not) do about it.

Some of this you probably already know: for investors with a sound long-term plan, the best action is often no action at all.

But that doesn’t mean sitting helplessly by.

You’ll learn why true diversification goes far beyond owning the S&P 500, how volatility drag quietly erodes your compounded returns even when your average return looks fine, and why disciplined rebalancing is actually a way of “buying the dip” without ever leaving the market.

We’ve also got a compelling case for redirecting your nervous energy: toward Roth conversions, estate planning, cash flow optimization, and other high-impact financial moves that are completely within your control.

Here’s what else we have for you in this episode:

- Why market timing is a losing game every time

- The real cost of missing the market’s best days (and why they cluster right next to the worst days)

- What “true diversification” actually looks like (get out of here with your 3-index-fund approach or your S&P500 fund!)

- How volatility drag reduces your long-term wealth even with the same average return

- Why you should consider increasing contributions during a downturn, not pulling back

- The high-impact financial planning moves to make right now instead of stressing about your portfolio

- How clients with financial plans weather market storms vs. those without

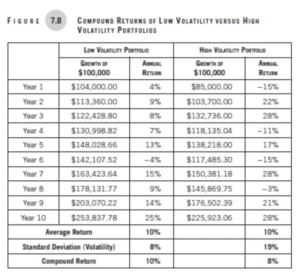

Don’t miss this resource mentioned: Chart on volatility drag from Peter Lazaroff’s Making Money:

KEY TAKEAWAYS

“Do nothing” is a strategy, not an excuse.

For investors with a well-constructed, long-term financial plan, the most powerful move during market volatility is often to stay the course. Reacting emotionally to short-term market swings almost always costs you in the long run.

Market timing is a loser’s game.

Historical S&P 500 data shows that whether markets just hit a new all-time high or just declined 10%, one-, three-, and five-year forward returns are all significantly positive on average. There’s no reliable signal telling you when to get out… and that’s only the first time you have to get it right. You also have to know when to get back in, making it even more unlikely that you’re going to nail this perfectly.

Missing the best days is devastating (and no one knows when they’ll be until after they’ve passed).

If you sell to avoid the bad days, you’re almost certain to miss the best ones too. The math on missing even a handful of those best days is severe enough to dramatically alter your long-term outcome.

The S&P 500 alone is not true diversification.

True diversification means global exposure: US large, mid, and small caps, developed international markets (Europe, Japan), and emerging markets (China, Korea, and beyond). Owning only the S&P left investors flat for an entire decade between 2000–2009. A globally diversified portfolio reduces your exposure to any single market’s extended downturn.

Volatility drag quietly destroys compounded returns.

Even if two portfolios have the same average return over time, the one with higher volatility ends up with less money. This is the mathematical case for managing volatility through diversification. It helps not just surviving volatility from an emotional standpoint, but protecting your actual wealth-building outcome.

Rebalancing is how you buy the dip without ever leaving the market.

A disciplined, rules-based rebalancing process automatically sells what’s risen and buys what’s fallen — keeping you invested and aligned with your risk tolerance at all times. You never have to guess when to jump back in, because you never jumped out.

Market downturns are the right time to increase contributions, not pause them.

Dollar cost averaging through volatile periods (or even increasing your contribution rate) puts more money to work at lower prices. Pulling back when markets are down means you miss the recovery.

Your financial plan is where real risk lives.

The biggest risks most people face aren’t portfolio-related. They’re things like: no estate plan, unfunded trusts, outdated beneficiary designations, and missed Roth conversion windows. These planning gaps can derail your financial future far more than a market drawdown.

Redirect nervous energy toward what you can control.

Instead of refreshing your portfolio app, use volatile periods to review your cash flow, optimize your tax strategy, fund your estate plan, and update beneficiary designations. These are high-leverage moves entirely within your control.

FAQs

Q: Should I sell my investments when the market is dropping?

A: Almost certainly not. The data supports that strongly. We cited historical S&P 500 data showing that whether the market just hit a new all-time high or dropped 10%, the one-, three-, and five-year forward returns average out to nearly identical positive numbers (roughly 10–14%). The moment you sell, you lock in your losses and face an even harder problem: figuring out exactly when to get back in. Most people who exit during downturns end up buying back in at a higher price — or missing the recovery entirely.

Q: What does “staying the course” actually mean in practice?

A: Staying the course means not making reactive changes to your investment strategy based on short-term market moves or emotional anxiety. In practice, it means keeping your contributions going, not shifting to cash, and trusting a long-term investment strategy that’s already been designed to survive periods of volatility. It does not mean ignoring your finances altogether. Instead, redirect your attention toward the planning activities that are actually in your control.

Q: If I can’t predict the market, is there anything I can do when volatility hits?

A: Yes! Here’s what IS in your control: reviewing and optimizing your cash flow, exploring Roth conversion opportunities (especially if you’re in a temporarily low-income period), funding your estate plan, updating beneficiary designations, and rebalancing your portfolio according to a rules-based process. These actions can have a significantly larger impact on your long-term financial outcome than any portfolio tweak.

Q: What is true diversification, and why does it matter right now?

A: A fully diversified equity portfolio might hold exposure to 5,000+ companies globally. This matters because when one sector or country is struggling, others may be holding steady or growing, reducing the overall volatility of your portfolio and protecting your compounded returns over time.

Q: What is “volatility drag” and how does it affect my money?

A: Volatility drag is the mathematical reality that higher portfolio swings reduce your actual compounded return — even if your average return looks the same on paper. Peter Lazaroff’s Making Money Simple has a chart that illustrates this clearly: two portfolios with the same 10-year average return end up with different actual balances, with the higher-volatility portfolio ending up worse off. This is one of the core arguments for why diversification isn’t just about emotional comfort. It’s a mathematical wealth-preservation strategy.

Q: Should I stop contributing to my investments during a downturn?

A: No! If you can, consider doing the opposite. When markets are down, your regular contributions buy more shares at lower prices (this is dollar cost averaging working in your favor). Emotionally, ramping up contributions during a downturn feels counterintuitive and scary. But looking at the long-term trajectory of markets, that’s precisely when putting more money to work tends to have the greatest impact. At minimum, don’t reduce contributions during market downturns.

Q: I’m closer to retirement — should I handle market volatility differently?

A: Somewhat, but perhaps not as dramatically as you’d think. Kali makes an important point: even if you’re in your 60s and plan to retire soon, if your money needs to last until age 85 or 90, a significant portion of your portfolio will still be invested for 20–30 years. That money still needs to work and grow. Sequence of return risk does matter is in the first five years of retirement; a sustained early downturn can accelerate how quickly a portfolio depletes. This is where a financial planner can help you structure income sources and withdrawals to protect you from that specific risk without abandoning growth potential altogether.

Q: How do I know if my financial plan is strong enough to hold through a period like this?

A: A strong plan is one that was built anticipating that volatility would happen — not one that assumed smooth sailing. If your plan includes a diversified, globally allocated portfolio, a clear savings and contribution rate, a rebalancing protocol, and a broader financial roadmap (tax strategy, estate plan, retirement income plan), then periods like this are what the plan was designed for. If you don’t have that in place, or you’re unsure, that’s the most important signal that it’s time to get one. Eric notes that his clients who have a plan in place rarely need to ask what to do during volatile markets — they already know.